Medicare is a valuable benefit, with average spending per beneficiary projected at $13,490 in 2018.1

Even so, Medicare covers only a little more than 60% of total health-care costs for Americans age 65 and older.2 Deductibles, copays, coinsurance, and payments for services not covered by Medicare can all add up to substantial out-of-pocket expenses. And there is no annual or lifetime out-of-pocket limit.

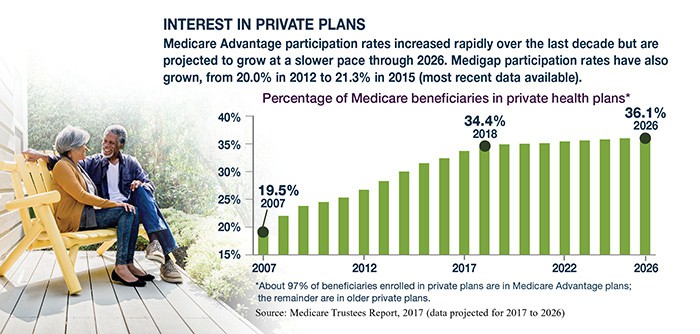

Whether you are enrolled in Medicare or planning to enroll in the future, you may want to consider two options to help manage out-of-pocket costs: Medigap and Medicare Advantage. Both are offered by private insurance companies approved and regulated by Medicare. They are mutually exclusive — you cannot be covered by both — but either might provide more stability to your health-care spending in retirement.

Supplemental Insurance

Medigap supplements coverage under Original Medicare Part A (hospital insurance) and Part B (medical insurance), and you must be enrolled in Part A and Part B in order to buy a Medigap policy. These policies pay all or a percentage of Medicare out-of-pocket costs such as deductibles, copays, and coinsurance. Some plans may pay for services not covered by Medicare, such as emergency medical care outside the United States (up to plan limits), but they generally do not cover long-term care, vision or dental care, hearing aids, or private-duty nursing. New Medigap policies do not cover prescription drugs, so you must enroll in Medicare Part D if you want prescription drug coverage.

Medigap plans are identified in most states by the letters A through N (E, H, I, and J are no longer available) in order to make comparison easier for consumers. All plans may not be offered in every state or by every insurance company, but plans identified by the same letter should offer the same benefits, though monthly premiums may differ.

You can enroll in a Medigap plan at any time, but the best time to do so is during the initial Medigap open enrollment period — the six-month period that begins on the first day of the month in which you are 65 or older and enrolled in Medicare Part B. During this time, you can buy any Medigap policy a company sells in your state for the same premium the company charges to healthy enrollees, even if you have health problems. If you miss this opportunity, an insurance company can charge you more for coverage or refuse coverage altogether, depending on your health. Medigap policies are guaranteed renewable; once you are enrolled, you cannot be denied coverage or charged more than healthy enrollees due to changes in your health.

A Medigap policy covers only one individual, so spouses need separate policies if both want coverage.

All-in-One Coverage

Medicare Advantage plans, also called Medicare Part C, replace Original Medicare Part A and Part B and often offer prescription drug coverage, similar to Medicare Part D. They may offer additional benefits not covered by Original Medicare such as dental care, eyeglasses, and wellness programs. Hospice care is covered under Original Medicare even if you have Medicare Advantage.

By enrolling in a Medicare Advantage plan, you are opting to receive benefits through a private insurance company, although much of the funding comes from the federal government. You will typically pay your Medicare Part B premium and an additional Part C premium, depending on the plan. You may also have out-of-pocket deductibles, copays, and coinsurance. However, all Medicare Advantage plans have an annual out-of-pocket maximum.

You can enroll in a Medicare Advantage (MA) plan instead of Original Medicare during your initial Medicare enrollment period — the seven-month period beginning three months before the month you turn 65. (Special enrollment rules apply if you have health insurance through your own or your spouse’s employment.)

You can change coverage from Original Medicare to MA, or vice versa, or change between MA plans during Medicare’s Open Enrollment period from October 15 to December 7. You can change from MA to Original Medicare during the disenrollment period from January 1 to February 14. From December 8 to November 30 of the following year, you can make one switch to a top-rated “5-star” MA plan.

For more information on Medigap, Medicare Advantage, and enrollment periods, see Medicare.gov.