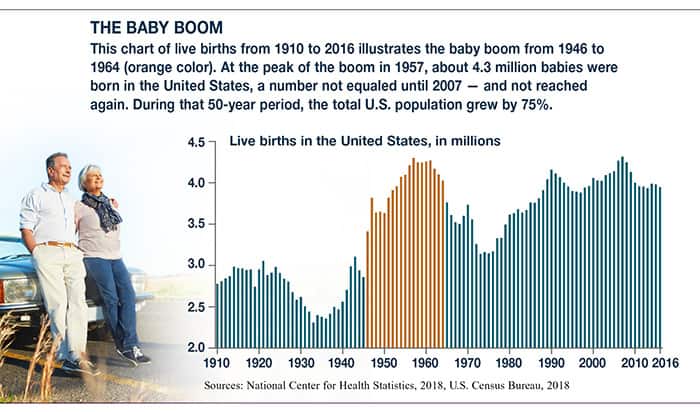

The baby boom generation was the largest and longest birth bonanza in U.S. history, extending 18 years from 1946 to 1964.1

With that wide spread, it’s natural that older baby boomers might have different feelings and experiences regarding retirement than younger boomers.

A recent survey highlights this disparity and raises important questions for those who are still in the workforce.

Happy Retirees

The good news is that retired boomers are generally happy with their retirement experiences. Six out of 10 say they feel better than expected about retirement, and three out of 10 say it’s about what they expected. Only 10% are disappointed or have negative feelings, typically citing financial stress.2

Three out of four said their financial situations at the time they retired were better or about the same as they expected. Only 23% did not meet their savings goals and had to adjust their spending. For many of them, reduced spending had not fundamentally changed their outlook on life, and closeness with friends and family often made up for lack of money.3

It’s worth noting that even those with sufficient assets were surprised by how much they spent on health care, travel, and taxes.4

Worried Workers

By contrast, 59% of working Americans across all ages — and 65% of working boomers — said that worrying about having enough money in retirement was one of their top financial concerns. Only 27% of retired boomers said the same.5

Some of this difference might be due to fear of the unknown. While you are still working, the idea of living without a paycheck may seem daunting, even if you have a solid savings balance. Working boomers were more nervous about money than retirees even when both groups had similar nest eggs.6

However, there are some fundamental differences in financial experiences on the two ends of the boomer generation that are worth considering.

Declining pensions. In 1975, when many older boomers had entered the workforce, 88% of private-sector employees had a pension. By 2017, that had fallen to 33%. And many plans were frozen with reduced benefits after 2006.7 Younger boomers are more likely to depend on income from a 401(k) plan, which places more responsibility on the worker for savings and potential retirement income.

Less favorable Social Security benefits. While full retirement age (FRA) is 66 for boomers born from 1946 to 1954, it increases by two months each year for those born from 1955 to 1959, and reaches 67 for those born in 1960 and later. This not only means younger boomers have to wait longer to collect full benefits, but it also reduces benefit percentages at other ages because they are based on FRA. Also, boomers born after January 1, 1954, cannot take advantage of a strategy in which one spouse files a restricted application for spousal benefits while continuing to earn delayed retirement credits to increase his or her worker benefit.

Rising college costs. People have children at different ages, but, in general, younger boomers have faced higher inflation-adjusted college costs that may have reduced the income available for retirement savings. They are also more likely to have provided their children with support after college.8

Higher long-term care costs. With longer life spans and rising long-term care costs, younger boomers also may face financial challenges helping their parents, or helping children and parents at the same time — a financial squeeze that gave rise to the term “sandwich generation.”9

If you are at the younger end of the baby boom generation, this may sound discouraging, but every generation faces challenges. No matter how many years you have before retirement, it’s wise to take a clear look at your strategy and make appropriate adjustments to put you on solid ground when it comes time to leave the workforce.