Crude oil plays an important role in the manufacturing and worldwide distribution of numerous products ranging from food to electronics.

When rising fuel costs are passed on to consumers, it can drive up inflation and reduce the purchasing power of wages. Gasoline and heating oil (which are derived from crude) are essential expenses for many households, so when prices spike there is less money available to spend on other goods and services. And altogether, consumer spending accounts for about two-thirds of U.S. gross domestic product (GDP).

For these reasons, high oil prices have long been blamed for driving down GDP growth, and it was widely assumed that low prices would provide an economic boost. But this relationship has become more complicated in recent years, largely because the United States has expanded its presence in the global oil market.

What Changed?

Starting in the mid-2000s, new technologies including seismic imaging, hydraulic fracturing, and horizontal drilling have allowed U.S. producers to extract more oil from shale deposits that were once thought to be depleted.

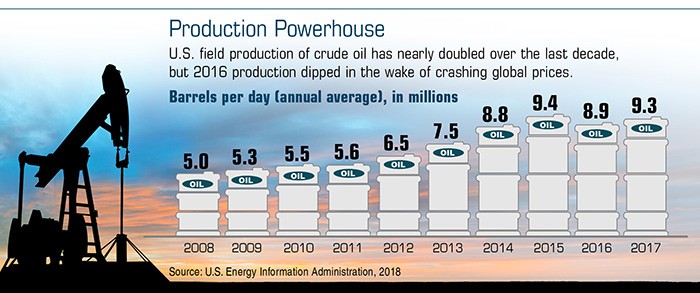

As a result, domestic oil production has nearly doubled over the last decade, and producers are now pumping more than 10 million barrels a day, surpassing a record set in 1970. The United States has also become the world’s top oil-producing nation and was responsible for 15% of the world’s total in 2016. Saudi Arabia and Russia follow close behind with 13% and 12%, respectively.1

Now that the United States is less dependent on foreign oil, domestic fuel prices may be less sensitive to geopolitical crises and supply shocks than they were in the past. On the other hand, the industry now employs more workers and is a larger contributor to the U.S. economy. So when market conditions arise that are problematic for oil producers — including low global oil prices — it could also have a negative impact on the nation’s GDP growth.2

Oversupply Story

Brent crude, the benchmark for global oil prices, dropped more than 70% between June 2014 and February 2016 due to an unexpected oil glut.3 U.S. oil production was surging while demand was falling, largely due to global economic weakness in Asia and Europe. U.S. consumers benefited from fuel savings, but domestic oil companies were forced to cut costs, shed workers, and put the brakes on investments in exploration and the drilling of new wells.4

Meanwhile, the Organization of the Petroleum Exporting Countries (OPEC), a cartel of 12 oil-producing nations, initially decided that preserving market share was more important than supporting prices by slowing production.5

Saudi Arabia and other key OPEC members eventually entered into an agreement with Russia to collectively cut production by about 1.8 million barrels per day through 2018.6 This was viewed as a positive step toward normalizing oil inventories, and Brent prices rose nearly 30% in the second half of 2017.7

By one estimate, the pullback in energy investment reduced GDP growth by 1.0% in 2015 and 0.5% in 2016, before rising oil prices helped U.S. producers recover, adding an estimated 0.5% to U.S. GDP growth in 2017.8

Exports Enter the Equation

Domestic oil exports were prohibited by U.S. law until 2015, but overseas shipments have been ramping up quickly. U.S. oil exports are now projected to more than double to 4.9 million barrels per day by 2023.9

Becoming a dominant oil producer and exporter may allow the United States to have more control over its own economic destiny. For example, global oil prices may be influenced less by OPEC’s production decisions and more by how quickly U.S. producers can ramp up or down to meet ever-changing demand levels.