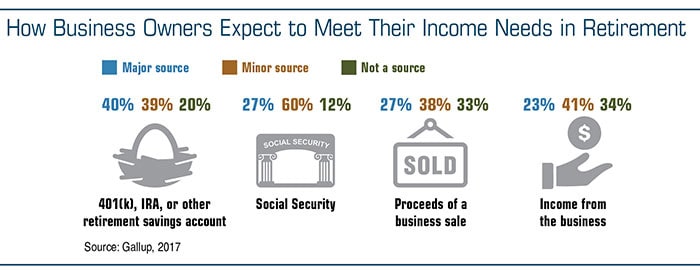

Like most business owners, you may devote most of your time, energy, and profits to running and growing your company. But keep in mind that you are likely on your own when it comes to saving money for retirement.

This is not the only reason it may be worth the effort to divert a sizable chunk of your earnings into tax-deferred retirement accounts. Doing so generally reduces your taxable income.

Better yet, both of the following types of retirement plans are relatively simple and inexpensive for small-business owners (with no employees) and self-employed individuals to set up.

Solo 401(k)

A solo 401(k) is a one-participant plan for business owners who have no other employees. Tax-deductible (or pre-tax) contributions to an individual 401(k) can be made in two ways.

As the employee, you can contribute as much as 100% of your annual compensation, up to the $18,000 annual maximum in 2017 ($24,000 if you are age 50 or older). In 2018, the limit increases to $18,500 ($24,500 if you are age 50 or older).

As the employer, you can also contribute an additional 20% of your earnings (25% if the business is incorporated) and deduct it as a business expense. Total contributions are capped at $54,000 in 2017, or $60,000 for those age 50 and older. In 2018, total contributions are capped at $55,000 ($61,000 if age 50 or older). A solo 401(k) plan may also allow plan loans and/or hardship withdrawals.

The deadline to establish an individual 401(k) and formally elect salary deferrals is December 31 of the year in which you want to receive the tax deduction (or before fiscal year-end for corporations). For businesses taxed as sole proprietors and partnerships, salary deferrals and profit-sharing contributions for 2017 must be deposited into the account by the April 17, 2018, personal tax filing deadline (October 15 if an extension was filed).

SEP IRA

Self-employed individuals can contribute 20% of their net earnings, up to $54,000 in 2017 (up to $55,000 in 2018), to a Simplified Employee Pension (SEP) plan. A SEP IRA may also be an appropriate choice for business owners with a small number of lower-paid employees. The same percentage of salary (up to 25% of compensation or $54,000 in 2017; or up to $55,000 in 2018) must be contributed to each eligible employee’s SEP IRA, including the owner’s. However, the business is not required to contribute every year.

You have until the due date of your business’s federal income tax return (including extensions) to set up a SEP IRA and make contributions.

Distributions from 401(k) plans and SEP IRAs are taxed as ordinary income. Early withdrawals (prior to age 59½) may be subject to a 10% federal income tax penalty.